Latest:

Protect Yourself from Scams and Fraud

You are here:

•

•

Will the US Equity Market Handle Large Scale Financing?

A Straits' Perspective

Will the US Equity Market Handle Large Scale Financing?

Dr. Hou

|

June 25, 2026

|

10 Minutes

AI is reshaping Wall Street's appetite for cash. As SpaceX gears up for the largest IPO in history, this month's commentary unpacks why financing, not earnings, may be the real test for US stocks ahead.

Summary

Driven by a surge in AI-related capex among US firms, US tech companies' free cash flow has declined noticeably. At the same time, major IPOs like SpaceX, along with a wave of equity and bond issuances, are expected to drive significant demand for capital across US markets from June onward. Over the past three months, stock prices have largely increased in the earnings growth of AI hardware companies. However, the market has not fully factored in the sustained heavy pressure on financing from AI capex.

US stock buybacks have exceeded equity financing and major shareholder selling every year over the past 17 years, yet this trend is likely to reverse in the second half of this year.

SpaceX will be included in the Nasdaq Index just 15 days after its IPO. Passive index funds such as ETFs will make mandatory allocations to the stock component and liquidate other index components accordingly. Therefore, the more capital chases SpaceX, the heavier the near-term selling pressure on other Nasdaq components.

Meanwhile, the net issuance of US Treasury bonds from June through year-end will double to $1.4trillion. Against this backdrop, Powell announced before his departure that the Fed would scale down RMP T-bill purchases from $40 billion to $10 billion per month starting in June. Incoming Chair Walsh has long opposed the Fed's balance sheet expansion, so additional liquidity support for US stocks from the Fed is unlikely in the near term.

Weaker economic data in April does not alter China's policy stance. With declining demand for loans from both households and corporates, the Chinese government did not adopt the usual approach of increasing government-led investment and financing efforts to boost the economy in May.

We expect the US capital markets to face severe liquidity pressures in June. Active traders may reduce their US stock holdings in the near term, especially tech hardware stocks that have previously posted steep gains. Long-term allocation investors may consider temporarily rotating into high-dividend, low-gain defensive stocks outside the Nasdaq Index, favoring sectors such as utilities, consumer staples, and healthcare.

US treasury bonds, precious metals, digital currencies, and other major commodities will also face capital outflow pressure. As such, these assets cannot serve as safe havens amid a US stock market decline driven by liquidity crunches. The A-share market has already entered a correction phase.

Previous Views:

AI investment has become the sole decisive factor driving the current global market. Still, it deepens the K-shaped divergence, widening earnings and market caps across sectors and individual stocks. China's economy continues to be driven more by industrial output and exports than by domestic consumption and demand.

Views in June:

I. Rising Financing Demand Is the Major Risk Facing the US Stock Market

In our previous month's report, we put forward the view that AI capex is the main support for the current US economy and US stock market. However, due to rapid growth in US AI capex, free cash flow for US-listed companies is declining significantly. At the same time, three AI-related giants plan to go public via IPOs to raise funds from June to the end of this year, SpaceX, OpenAI, and Anthropic. The total valuation of these three unlisted companies is currently close to $4 trillion. Previously, the five major cloud service providers, where US AI capex is most concentrated - Google, Microsoft, Amazon, Meta, and Oracle - have raised combined bond financing of more than $80 billion per quarter in the past three quarters. Moreover, Google launched an $85 billion stock offering in May, and Meta also has plans to issue additional shares in the next few months. In May, ahead of their IPOs, Open AI and Anthropic raised $40 billion and $60 billion, in equity financing from the private market, respectively.

The recent wave of large equity and bond financing reflects the substantial funding requirements of major technology companies as they aggressively increase AI investment. Although the stock market still firmly believes in the prospects and corporate profits depicted by AI technology companies, the reality is that such successive large financings have caused a continuous and significant "blood-draining effect" on cash flows in secondary capital markets. We believe this is the most substantial risk the US stock market may face from June till the end of this year.

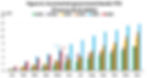

Throughout this 17-year bull market in US stocks, there have been ups and downs in economic growth, as well as unexpected risk events such as the European debt crisis, the Covid-19 pandemic, and the Russia-Ukraine war. Overall, a constant factor supporting the US stock market is that the annual amount of corporate stock repurchases is greater than the amount of stock supply brought by corporate IPOs, follow-on share offerings, rights issues, and major shareholders' sales (Figure 1). Over the past 17 years, the US stock market has never provided net financing, leading to the continuous and extreme amplification of its investment attributes, while the financing function has stagnated. In fact, in previous years, the net financing amount for US stocks could not keep pace with the scale of stock financing in China's "A-share + Hong Kong" stock market.

However, the rapid expansion of this round of AI capex, which began in the fourth quarter of last year, is reshaping the US stock market, and the listing of SpaceX will be a landmark event in this shift. First, SpaceX, which is scheduled to go public in June, is expected to raise between $75 billion and $86 billion in its IPO, which will be the largest IPO in human history, several times larger than the previous largest IPO's financing amount. Moreover, the number of new shares issued in SpaceX's IPO is expected to be around 550 million. In addition, within 30 to 180 days after its listing, 4.5 billion additional Class A old shares will be unlocked and allowed to be sold in the secondary market. Based on its IPO offering price, the total market value of SpaceX's unlocked and tradable Class A shares will exceed $700 billion by the end of this year. The total amount of share buyback plans announced by US listed companies in the second half of this year is about $650 billion.

If we add other IPOs and additional share issuances, we believe that from June till the end of the year, US stock market supply is likely to exceed repurchases for the first time since 2009. In other words, in the past 17 years, the US stock market has become a "net financing market" for the first time in H2 this year. The A-share and Hong Kong markets have long operated as net financing markets, which typically command lower valuations than investment-led markets such as the US. If the US market were to experience a similar shift, even for a relatively short period, the current high valuations and liquidity premiums could come under pressure, increasing market risks.

In addition, the significant increase in US AI capex over the past two quarters has led to a substantial rise in revenues in related US industries, especially in the semiconductor hardware industry. However, the stock market has primarily increased in this year's profit growth in its earnings forecasts and valuations. The Philadelphia Semiconductor Index nearly doubled after its March 30 trough, largely reflecting this significant growth in profitability. But excluding the computer and electronic equipment industry, the revenue and order conditions of other US manufacturing industries have not improved significantly (Figure 2), indicating that current market strength is highly concentrated in companies directly benefiting from increased AI capex, such as those in the semiconductor hardware sector.

As we analyzed earlier, the current increase in US AI capex has exceeded the level that corporate free operating cash flow can cover, leading to increasing reliance on capital market financing. Therefore, if market volatility rises or financing becomes harder to obtain, the AI investment cycle could slow. Despite robust long-term order books, upstream semiconductor and hardware companies may still face challenges in delivering the earnings and cash flow growth implied by current market valuations. Major AI-models and computing-power providers now care less about costs, increasing investment to gain a competitive edge, which is driving up the costs of building computing capacity and producing tokens. This may instead make it more difficult for the AI industry chain to achieve its own operating cash flow balance in the future.

Due to the unanimous optimism about new technologies and products, market investment surged, resulting in short-term shortages and soaring prices for upstream raw materials and components. This in turn makes it harder for downstream products to achieve their own profitability and operating cash flow balance in the future. While AI may have huge prospects for future applications, but its capex, and upstream costs are also far higher than those of sectors like solar, wind power, and new energy vehicles. However, household income will never grow as rapidly in the short term as the growth rate of capex on new technologies and products. Therefore, once the total amount of capex becomes too large, the contradiction between the explosive growth of such capex and the stable, low growth of household income will soon become a problem, leading to the bursting of asset price bubbles and a downcycle in the capex cycle. This is a pattern that almost every new technology capex cycle goes through. It is not difficult to conclude that the larger the total capex, the worse the sustainability of its high growth. Currently, annual AI capex has reached $1 trillion, while US households' wage income in 2025 was $15.6 trillion. In China, after the total capex on solar, wind power, new energy equipment, and automobiles reached RMB2 trillion per year, which is about 4% of Chinese households' wage income, there was a sharp slowdown in growth.

II. Where Will the Money Come From?

As for the argument about the balance between revenue and costs in the AI industry, it may take longer to reach a clear conclusion. However, in terms of the financing pressure in the capital markets, it is an urgent issue at present. SpaceX has already launched its offer and is expected to arrive on June 12. Moreover, after intensive communication by SpaceX's senior management, the Nasdaq Stock Exchange approved in May a revision of its rules for including mega-cap companies in the Nasdaq index. The new rules allow companies like SpaceX, which are not yet profitable, to be included in the index just 15 days after listing, with their index weight calculated as three times their floating market capitalization. This will undoubtedly force many ETFs and index funds that passively track the Nasdaq index to buy SpaceX shares after its listing. However, as passive funds are unlikely to receive significant new inflows in the short term, they may need to sell existing Nasdaq holdings to fund purchases of SpaceX shares. As a result, the largest constituents of the Nasdaq index are likely to be among the first stocks to face selling pressure following SpaceX's listing.

Thirty days after listing, approximately 900 million SpaceX shares will be unlocked. This will force passive index funds to increase their purchases further as SpaceX's floating market capitalization rises. On the other hand, early investors holding Class A shares may engage in large-scale selling and cashing out, i.e. withdrawing funds from the secondary stock market, causing an actual "blood loss" in the stock market.

The peak issuance of US treasury bonds will also arrive in the second half of the year. Since corporate and personal tax settlements in the US usually occur from January to April, treasury bond supply is typically concentrated from May to December. From January to May this year, net US Treasury bond issuance was approximately $700 billion (Figure 3). According to the US Treasury Department's estimate, US Treasury bond financing from June through the end of the year will be around $1.4 trillion, twice the total financing in the first five months of this year.

Given that, after June this year, the market will witness massive stock and corporate bond financing, as well as much higher demand for US treasury bond financing than in the first five months, whether the Fed can provide sufficient liquidity support promptly has become a key question to watch. However, judging from the statement made by Jerome Powell, who has just stepped down as Fed Chair at the May meeting, he promised to significantly scale back the RMP program launched in early December last year: starting in June, the Fed will reduce RMP from $40 billion per month to $10 billion per month. According to data released by the Fed, the Fed's RMP program has led to a substantial increase in its holdings of US short-term T-bills from $195.5 billion in December last year to $469.5 billion, meaning it has increased its holdings of T-bills by $274 billion over just six months. This is also the direct reason why US commercial banks have expanded their balance sheets by $1 trillion in the past six months (Figure 4).

Looking at the asset side of the US commercial bank balance sheet, the biggest beneficiaries of the balance sheet expansion driven by the Fed's RMP over the past six months have been the stock market and corporate loans. At the same time, the total amount of commercial and industrial loans held by commercial banks has increased by more than $200 billion, equivalent to an annualized year-on-year growth rate of 15%, and a large portion of this incremental lending has flowed into AI-related capex. Other items such as consumer loans, MBS, and treasury debt, have also increased, but their growth rates are much lower.

However, with the change in Fed Chair, the new Chair Kevin Warsh, has always consistently opposed the Fed's balance sheet expansion. Therefore, we expect that "where will the money come from?" will become a major issue weighing on the US capital market for some time to come.

III. Weaker Economic Data in April Does Not Alter China’s Policy Stance

As we mentioned in our previous monthly report, China's economy still maintains a pattern in which output outperforms consumption and external demand outperforms domestic demand. However, unlike in the past two years, the current Chinese government has not adopted a pro-stimulus policy stance to accelerate the expansion of the fiscal deficit. In terms of government bond issuance data, including treasury bonds and local government bonds, the cumulative net issuance from January to May this year was RMB 5.76 trillion, a year-on-year decrease of 10% from RMB 6.38 trillion in the same period last year (Figure 6).

This indicates that despite the weakening of various domestic economic indicators in April, the implementation of overall domestic macro policies in May did not change significantly. However, the financing data for both households and corporations in April showed a relatively clear weakening. Nevertheless, in April this year, for the first time in history, the total amount of YTD new medium- and long-term household loans turned negative (Figure 7). However, even under such circumstances, the Chinese government did not adopt the usual approach of increasing government-led investment and financing efforts in the short term to boost the economy in May. This indicates that the Chinese government still maintains strong policy resolve and confidence.

On the positive side, the overall liquidity conditions in banks and the capital market remains relatively loose. In addition, the government has recently stepped up efforts to restrict the illegal flow of domestic capital into foreign investment markets. Therefore, if US stocks decline in the future due to insufficient capital liquidity, the overall impact on China's stock market will be relatively small.

IV. Market Strategy

With large IPOs like SpaceX, numerous tech companies planning to raise additional capex funds via equity offerings or corporate bond issuances, and a surge in US treasury issuances scheduled for 2H of this year, we expect the US capital markets to face severe liquidity pressures starting in June. If SpaceX completes its IPO at a high valuation and continues to draw substantial speculative capital after listing, overall market liquidity risks will further escalate, particularly for other major Nasdaq component stocks.

US treasury bonds, precious metals, digital currencies, and other major commodities will face pressure from capital outflows. As such, these assets cannot serve as safe havens amid a US stock market decline driven by liquidity crunches. The A-share market has already entered a correction phase. While the broader benchmark indices are likely to see limited downside, tech hardware stocks that rallied alongside US equities earlier are also facing substantial to pull back pressure.

Dr. Hou

Dr. Hou holds an MBA from Wisconsin School of Business at the University of Wisconsin-Madison and has a rich history of leading strategy teams. At China International Capital Corporation, he was instrumental in guiding both the overseas and A-share strategy teams, earning several top honors in strategy research. Later, he significantly contributed to macro strategy research at Shanghai Discovering Investment, where he played a pivotal role in achieving exceptional market returns. His expertise is particulary recognized in financial strategy and market analysis within the chinese market.

Edited by the Straits Financial Group Content Team

DISCLAIMER: This document is issued for information purposes only. This document is not intended, and should not under any circumstances to be construed as an offer or solicitation to buy or sell, nor financial advice or recommendation in relation to any capital market product. All the information contained herein is based on publicly available information and has been obtained from sources that Straits Financial believes to be reliable and correct at the time of publishing this document.

Straits Financial will not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Past performance or historical record of futures contracts, derivatives contracts, and commodities is not indicative of the future performance. The information in this document is subject to change without notice.

Please also refer to our important notices at https://www.straitsfinancial.com/important-notices-and-disclaimer.

Chief Economist Commentary

Explore More Commentary

Stay informed with our Chief Economist's monthly perspective on critical economic trends and market movements.

A Straits' Perspective

AI Investment Is a Key Driver of Stock Market Trends

May 20, 2026

|

10 Minutes

AI investment is becoming an increasingly visible factor in global stock market movements as technology-related sectors expand. Investment activity tied to artificial intelligence infrastructure, computing systems, and digital services continues to influence how markets assess long term growth opportunities.

A Straits' Perspective

“Iran War” Could Pose a Threat to the Global Economy

March 16, 2026

|

20 minutes

Rising tensions involving Iran, the United States, and Israel could pose significant risks to the global economy and financial markets. Escalation of conflict in the region may disrupt energy supply chains, increase volatility in oil prices, and threaten critical shipping routes such as the Strait of Hormuz.

A Straits' Perspective

How We View the “Warsh Turbulence”?

February 13, 2026

|

20 minutes

The nomination of Kevin Warsh has introduced uncertainty over US monetary policy and liquidity trends. We analyze the practicality of QT under current fiscal conditions and outline our market outlook for US stocks, China’s A-share market, and major commodities.